Abstract

The main focus of this survey is to examine the key determinants of loan consumption in Kenya, with a keen focus on variables such as monthly expenditure per adult, deposits, economic strength index, and diverse economic opportunities. The study's target population is Kenyan citizens aged 18 years and above. The study obtains data from the Kenya national census, aggregated at the county level. The literature review section presents sufficient support for the study’s hypothesis. In particular, the authors highlight Kenya as a country with one of the highest loan consumption in Africa, which plays as a motivation for conducting this survey. The survey methodology involves the use of quantitative analysis using descriptive statistics like tables, graphs and charts, deterministic multiple linear regression, and stochastic analysis through Monte Carlo simulation. The results of the survey show that monthly expenditure per adult, deposits, and economic strength index have a significant impact on loan consumption amount; that is, R-squared is equal to 0.88. The implication of this survey is based on its contribution to the understanding of loan consumption behaviors in Kenya, presenting relevant insights for policymakers, financial institutions, and other stakeholders in the lending and borrowing processes. The outcome has the potential to inform loan structure policies to enhance the promotion of responsible and sustainable loan consumption.

Keywords

Multiple Linear Regression, Stochastic Analysis, Monte Carlo Methods, Descriptive Statistics, Loan Consumption, Economic Strength Index

1. Introduction

Loans and credit facilities are one of the ways that have been used by government and financial institutions to aid in fighting unemployment and promote livelihood. Loaning had over the years gained credibility in the major banking institutions plus ensuring rise in many micro-finance institutions and cooperatives that offer wide range of services among them being credit facilities.

As a result of increasing loan consumption, Kenya has continued to experience rising growth rate in the number of micro small and medium enterprises (MSMEs) over the years. For instance, in 2018 alone, according to the Kenya SME Performance Index 2019, the SME growth rate was at 6.3

.

For so many times it has been argued that the supply and demand for loans is correlated with the economic status of a place. In the study to investigate factors that influence the demand for credit among small-scale investors, the authors found that economic status and demand for loans have a strong correlation, thus when the economy is growing, the demand for loans also becomes high

| [32] | Priscilla N. Wangai, B. M. (2011). Factors that Influence the Demand for Credit for Credit Among SmallScale Investors: a case study of Meru Central District, Kenya. Retrieved from https://core.ac.uk/download/pdf/234629179.pdf |

[32]

. Economists also argue that the correlation is attributed to the fact that in a growing economy, many projects are more profitable, implying that the aspects where one can invest are also many compared to a slowly growing economy. The majority of business analysts and economists tend to view the loan market in a traditional supply and demand framework that considers alternate ways to source business funding and control capital to invest

| [39] | Weiss. (2008). Credit Rationing in rural India. Journal of Economic Development, 23-45. |

[39]

.

Kenya is a country with one of the highest loan consumption rates in Africa. Kenya is the third highest country in loan uptake in Africa after Nigeria and South Africa

. With the ever-increasing percentage of loan uptake, one of the risks that Kenya has been facing is increasing in non-performing loans, which may be a discouraging factor to lenders. Since the beginning of the new millennium, despite the rising number of people going for loans, Kenyan lenders have been working hard to ensure that the public has sufficient information that can lead to a reduction of non-performing loans. These efforts have proven to be bearing fruits if a study by Central Bank of Kenya, is something to go by

| [5] | Central Bank of Kenya. (2017). THE BANKING (PENALTIES) REGULATIONS, 2017. Nairobi: Central bank of Kenya. |

[5]

. According to this study, the non-performing loans as a percentage of the total loans stood at 13%.

Banking, Microfinance, and other financial institutions have been instrumental in promoting livelihood, startup businesses, and other social sectors through different services such as savings services, loans, and financial literacy training, among others. As opposed to other banking services, loan services had experienced criticism for a very long time before gradually becoming more accepted in Kenya

| [15] | Johnson, S., & Arnold, S. (2012). Inclusive Financial Markets: Is Transformation Underway in Kenya? Development Policy Review, 30(6), 719-748. |

[15]

. Loans are a very critical service for both the growth of an individual lender, the borrower, and the economy’s financial environment. According to the International Journal of Current Research

| [35] | Syomane, Felix S.; Dr. Michael, Wahome;. (2018). Financial Institutions Factors Influencing Loan Default by SMEs in Kitui County. Nairobi: INTERNATIONAL JOURNAL. |

[35]

, one of the reasons individuals and SMEs fear engaging in loan uptake is fear of defaulting, which the research said was attributed to constrained irregular income, SMEs’ poor management, and competition from financially established entities. In an investigation of factors affecting loan repayment in Kenya, it was established that the loan repayment trend is significantly associated with “Individual borrower’s” attributes and “group” attributes

. These studies, among many studies, concentrated on either loan defaulting habits or loan repayment habits. However, there is very limited information on loan uptake habits. This study therefore seeks to investigate factors influencing loan uptake in Kenya. In particular, the study models monthly expenditure per adult, deposits, economic strength index, and diverse economic opportunities, to determine which of them are significant in predicting loan consumption in Kenya.

The data used in the study is obtained from the census data for existing loans in Kenya, to fill the knowledge gap on the determinants of loan consumption in Kenya.

2. Literature Review

Loan consumption in Kenya is a multifaceted issue influenced by a combination of economic, social, institutional, individual, technological, environmental, governmental, and behavioral factors. In this section, we assess the theoretical and empirical literature reviews. In the theoretical review, we look at several theories that can be useful in explaining factors that influence loan uptake. In the Empirical review, we explain past research work conducted and provide research gaps about the factors influencing loan uptake.

Theoretical Literature Review

Loanable Fund Theory

This theory explains the relationship between interest rates and loanable funds. This theory originated from the Swedish economist Knut Wicksell

| [16] | Kumar, M. (2018). Loanable Funds Theory (With Diagram). Washington DC: Economics discussion. |

[16]

. The theory argues that the supply of loanable funds and loan demand influence interest rates. According to this theory, there is a positive association between demand for loanable funds and interest rates. Supply of loanable funds and interest rates also have a positive association according to this theory. As opposed to the general belief that interest rate determines the rate of loan uptake, this theory implies that the opposite is true; the interest rate is determined by the supply and demand for loanable funds

| [25] | Mutezo. (2005). Obstacles in the access to SMME finance. Pretoria: University of South Africa. |

[25]

. In other terms, the interest rate is determined by the rate of loan uptake. According to this theory, demand for loanable funds is dependent on these three factors namely:

Investment: In this theory, the major source of demand for loans is the need for investment.

defined investment as the expenditure geared towards the making of new capital goods, inventories, and processes, to make profits. Connecting this to our areas of interest, it is therefore to assess whether local areas with more investment opportunities are likely to have higher loan uptake or not.

Another factor is hoarding. Hoarding is defined as the persistent obstacle in discarding possessions, irrespective of their actual value

. The loanable fund theory claims that demand for loans may also arise due to the need to hoard the loan as idle cash balances to satisfy liquidity desires. The theory claims that there is a decreasing association between the hoarding purpose and interest rate.

The third factor is dissaving. Dissaving is the opposite of the practice of saving. It is synonymous with regular withdrawal. This theory argues that loan demand also comes as a result of people wanting to spend beyond their normal income. For instance, in our study, one of the factors that we are trying to assess its relationship with loan uptake is adult expenditure. This theory explains that when there is a need for people to spend more beyond their income, there is likely to be an increase in loan taking.

It is important to note that the loanable funds market is a compromise of both the lenders of the loan and the borrowers. While these forces are essential in determining the interest rate of the loan, it is also important to assess factors that are essential in determining the forces behind loanable funds

. The demand and supply of loanable amounts will always balance at a given interest rate. Interest rates always differ from one market to another depending on market conditions. Likewise, the supply and demand of loans also vary based on market conditions such as the Economic strength index and diverse economic opportunities.

This theory also talks about dissaving as a determinant of the demand for loanable funds. Given that dissaving is negatively associated with deposits while positively associated with expenditure, therefore a need to assess if there is any relationship between money deposited and loan demand, as well as the relationship between adult expenditure and the loan demand.

Liquidity Preference Theory of Credit

The liquidity theory of credit was first put forward by John Maynard Keynes. The theory suggests that the demand for money does not lie in borrowing but in its desire to remain liquid

. The main purpose of this theory is to explain the role interest rates play in supply and demand for money. This theory explains money demand in three perspectives namely transaction, precautionary, and speculative. The theory argues that the most liquid asset in an entity is money and thus how liquid an asset is, is measured based on how quickly the asset can be converted into cash.

Based on this theory, people like being liquid due to the expenses incurred on a day-to-day activity. This theory states that the desired level of liquidity is dependent on the income level. This is to say that if the income of an individual increases, then the spending also increases thus more money is required for increased spending. This type of liquidity is what is referred to as transaction demand.

As we had seen in the previous theory, loan demand might increase due to increased spending. Relating to this, we can say that increased income might lead to the need for more money for increased spending and therefore more likely to increase the loan demand. People with high expenditure may need to borrow to facilitate their expenditure

| [34] | Rehan Azam, M. D. (2012). The significance of socioeconomic factors on personal loan decision. Munich: Munich Personal RePEc Archive. |

[34]

.

Another type of liquidity demand is the precautionary demand. This type of demand increases with an increase in the income level of an individual. This demand for liquidity covers the unforeseen expenditure. In other words, it is a demand for money that can cover risks that cannot be predicted. This includes money to cover accidents, sicknesses, political violence and instability, drought, floods, etc., to cover for these uncertainties, many individuals take loans that are then invested in such demands. Based on the theory of liquidity preference, it is possible to control the interest rates thus growth in loan demand and thus creation of employment and empowerment

| [36] | Tilly, G. (2006). Keyne's theory of liquidity preference and his debt management and monetary policies. Cambridge journal of Economics, 657-670. |

[36]

.

The last type of liquidity demand is speculative demand. This demand takes into consideration future changes in the interest rates. Keynes indicated that this demand has a negative association with the rate of interest. That is, if the rate of interest goes up, it results into lower price of speculative demand for capital. This was explained that when the rate of interest is lower, people tend to take more loans so that they may be cushioned in case of higher interest rates in the future

| [36] | Tilly, G. (2006). Keyne's theory of liquidity preference and his debt management and monetary policies. Cambridge journal of Economics, 657-670. |

[36]

.

Harry Markowitz’s Modern Portfolio Theory

Markowitz’s modern portfolio theory is aimed at maximizing expected return for a given amount of risk, through carefully selecting the proportions of several assets. This theory is based on the need to apply mathematics in analyzing the stock market. Before this theory, the investing process concentrated only on individual stock; an investor would look for an asset that would assure him/ her decent returns with minimal risk

.

Markowitz's modern portfolio theory allows an investor to mathematically trade-off open-mindedness and reward expectations, leading to the optimal portfolio. This formula is based on two concepts: That every investor’s objective is to maximize return for any level of risk and that the risk is reducible through spreading the portfolio through several securities. The theory assumes that investors will only consider a high-risk investment if the expected reward is larger than other lower-risk investments.

An example of modern portfolio theory in loan demand will be when an investor is considering between two loan facilities, loan A and loan B both at an interest rate of 6% per annum. However, loan As repayment period is twice as long as Loan Bs, implying that the investor will have twice longer period to pay the loan if he picks Loan A compared to Loan B. With a longer repayment period, it implies that the investor will be paying less money for loan A compared to loan B.

Based on the modern portfolio rationale the rational investor will always pick loan A as opposed to loan B since loan A will give flexibility and thus more return compared to loan B.

Applying Modern loan portfolio theory to our factors of interest, we can pick for example diverse economic opportunities. Given two lenders who are to choose between two localities to operate in, location A and location B with people of the same economic level but economic activities in A are more than the economic activities of B. A rational investor will prioritize locations A to B based on the portfolio theory.

Imperfect Information Theory

Most problems faced by financial institutions and other money-lending entities in the current world have been approached through the theory of imperfect information and imperfect administration problems. Imperfect information is where parties involved in a business have different information, an example is when the lender has more information about the terms of the loan than the borrower. The lenders always have better information about the policies than the borrowers since they are more familiar with them. Contrary, borrowers have limited information about the terms of operation. Likewise, the lender has limited information about the borrower’s inability to repay the loan while the borrower is more familiar with his/ her operations and has more information on whether he/she can successfully repay the loan or not

.

Two main problems may arise based on the lack of equal information for the parties involved in the contract. According to the theory, the incentive problem refers to the cost incurred by the lender to be assured that the borrower will repay the loans while the enforcement problem arises as a result of legal barriers to enforcing the repayment of the loan. For instance, there might be legal barriers when it comes to selling collateral. Regardless of the laid down protocols by the parties, all must lead to the repayment of loans and interests by the borrower. In a case where the loan is not repaid, the borrowers benefit at the expense of the lenders.

Asymmetrical Information Theory

The theory of asymmetrical information indicates that the lack of symmetrical information among two parties engaged in a business or contract is the major cause of poor operation in the financial market for developing economies such as Kenya. Asymmetric information arises when one party possesses more information or better information compared to the other party

. Where there is asymmetric information, this can result in adverse selection, unfinished markets, and market failure.

In the financial lending market, adverse selection can be explained as a borrower having more information about his/her financial situation than the lender. On the other hand, the lender has no certainty whether the borrower is likely to make full repayment or will default. Despite the efforts put in place by the lender to overcome this challenge such as looking at past credit history, evidence of reliable sources of income, and profitability of the project, the lender still will only be able to obtain limited information

.

Adverse selection will therefore lead to the lender charging higher rates to cushion the unforeseen risk. If there could be perfect information, then financial lending institutions may have no reason to charge higher premiums since they would be assured of timely repayments

. The authors argue that the following need to be considered to overcome asymmetric information:

The business entities need to put more investment into the business to give positive signals. If a business is a one-off private entity, it might raise suspicion. However, when the entity invests big in billboards, branding, and building assets, it gives a signal of being there to stay for the long term. Likewise in the money lending market, new clients with minimal savings might be likely to default on loans as compared to customers who have saved with the institution for a longer period.

Businesses that give warranties are likely to avoid doubts about asymmetric information. This is equivalent to a borrower giving collateral before being given a loan. When there is collateral, the lender is cushioned against loan default by the borrower thus preventing cases of adverse selection in the market.

The financial institution can also introduce bonuses for those borrowers who make repayments within time. For example, if say a lender gives X amount of money to a borrower at an interest rate of say 12% per annum. Then it happens that a borrower repays the amount before the elapse of the repayment period, as a motivation the lender can introduce a bonus that reduces the interest rate to say 6% for such a borrower. This will encourage borrowers to repay their loans in time to incur lower interest rates.

Balanced Scorecard Theory

Balanced scorecard theory tries to assess how lenders may obtain feedback on the business processes and external outcomes to continually improve the loan performance and reduce nonperformance loans

| [13] | Isoraite, M. (2008). THE BALANCED SCORECARD METHOD: FROM THEORY TO PRACTICE. INTELLECTUAL ECONOMICS, 18-28. |

[13]

. Performance management has become a legal requirement for all sectors. However, not many tools exist to effectively measure public and private service delivery

| [35] | Syomane, Felix S.; Dr. Michael, Wahome;. (2018). Financial Institutions Factors Influencing Loan Default by SMEs in Kitui County. Nairobi: INTERNATIONAL JOURNAL. |

[35]

. In the modern business market, employee skills, and customer and supplier relationships are key in giving a very important cutting-edge to any organization. The balanced scorecard method from the theory of balanced scorecard, translates an organization’s strategy into measurable performance objectives. This method is built on four key balanced approaches and connects them using the cause-and-effect concept. A thorough balanced scorecard is capable of predicting the effectiveness of an entity’s strategy through a series of connected performance measures centered on four perspectives which are finance, customers, internal processes, and employee learning and growth.

This approach has been widely used by lenders in the financial market to measure its performance among them being to measure and rate its customers based on different attributes. Based on the fact that the modern world is data-driven, a lender just like any other organization is keen on making informed decisions and avoids making decisions based on heuristics, and assumptions. A balanced scorecard measures the customers’ financial performance, their economic activities, reliability of their sources of income, and credit repayment history among many other key factors, and comes up with proper information that will be important when issuing the customer with loan.

Empirical Literature Review

Lending policies, including collateral requirements and credit history checks, can either facilitate or hinder loan consumption. Stringent credit policies are a barrier for many potential borrowers, especially small and medium enterprises (SMEs) and low-income individuals

| [3] | Beck, T., Demirguc-Kunt, A., & Martinez Peria, M. S. (2008). Banking Services for Everyone? Barriers to Bank Access and Use around the World. World Bank Economic Review, 22(3), 397-430. |

[3]

. Higher and stable incomes are associated with higher loan uptake due to the increased ability to repay. Additionally, a positive credit history enhances access to credit. A study by Johnson and Arnold found that individuals with higher income levels and good credit scores are more likely to secure loans

| [32] | Priscilla N. Wangai, B. M. (2011). Factors that Influence the Demand for Credit for Credit Among SmallScale Investors: a case study of Meru Central District, Kenya. Retrieved from https://core.ac.uk/download/pdf/234629179.pdf |

[32]

.

Ochung investigates the factors affecting loan repayment among customers of commercial banks in Kenya

. The study establishes that there is a significant relationship between group factors and loan repayment, individual borrower’s habit factors and loan repayment, and loan factors and loan repayment. The findings of the study lead to the recommendation that the bank should have mandatory supervision of borrowers on loan utilization and repayment and there is a need for banks to apply efficient and effective credit risk management to ensure that loans match the repayment ability and implement a credit information bureau where reference can be made before loan disbursement.

Cultural attitudes towards debt play a crucial role. In some Kenyan communities, borrowing is stigmatized, which can deter individuals from taking loans. Conversely, in cultures where borrowing is seen as a means to achieve economic progress, loan uptake is higher

.

Makorere investigate the factors affecting loan default in Tanzania

| [20] | Makorere. (2014). Factors Affecting loan default in Tanzania. Daresalam. |

[20]

. This study establishes the biggest percentage of borrowers; 32% of the respondents, are unable to repay their loans in time due to high interest rates. Therefore, borrowers were likely to borrow from financial institutions with low interest rates as compared to the ones with high interest rates.

On their part, Maina K. employ primary data collection using primary data-capturing questionnaires in assessing the institutional factors contributing to loan defaulting in MFIs in Kenya

| [19] | Maina, K. (2014). Assessing Institutional Factors contributing to loan defaulting in MFIs in Kenya. Nairobi. |

[19]

. The results of this study show that credit policies, loan recovery procedures, and loan appraisal methods are all significant in impacting the loan default rate.

Natural disasters and adverse environmental conditions can impact financial stability, affecting loan uptake. For example, droughts can reduce agricultural productivity and income, making it difficult for farmers to service loans

| [11] | Government of Kenya (GOK). (2018). Economic Survey 2018. |

[11]

.

The authors also explore an investigation on the causal relationship between bank loans and deposits and the efficiency of the use of loans and deposits in Vietnam's banking system

. The study establishes that bank deposits have a positive and significant impact on bank loans in the underdeveloped banking system. The study also reveals that deposit-taking and loan-creating activities are moderately well over the period under investigation. However, there is a need to do more deposit-taking activities in the future.

Policies aimed at enhancing financial inclusion, such as promoting digital financial services, have positively impacted loan uptake. The Financial Sector Deepening (FSD) Kenya reports that financial inclusion initiatives have significantly increased the number of people with access to credit

| [8] | Financial Sector Deepening (FSD) Kenya. (2014). The Growth of M-Shwari in Kenya – A Market Development Story. |

[8]

.

Access to banking and financial services is a primary factor. Regions with a higher density of financial institutions experience greater loan uptake

| [6] | Central Bank of Kenya. (2019). Bank Supervision Annual Report 2019. |

[6]

. Microfinance institutions (MFIs) and digital lending platforms have significantly improved access to credit in rural and underserved areas

| [21] | Mbiti, I., & Weil, D. N. (2011). Mobile Banking: The Impact of M-Pesa in Kenya. NBER Working Paper No. 17129. |

[21]

.

A study to assess the extent to which access to the women's enterprise fund program impacts socio-economic development revealed that women's enterprise fund program policies and procedures influence women's enterprise contribution to socio-economic development

| [27] | Obiero, S. O. (2020). Influence of Women Enterprise Fund on Socio-Economic Development; A case study of Lurambi Constituency. Nairobi: University of Nairobi. |

[27]

. The study uses a sample size of 100 women who are beneficiaries of the enterprise fund and applies a descriptive research method. Correlation and multiple linear regression analyses are applied at 0.05 significant levels in hypothesis testing.

Johnson and Arnold investigate how socio-cultural practices are influencing credit uptake behavior of Women-owned Micro-Enterprise Projects in Machakos Sub-County

| [14] | James MutukuNzeki, D. G. (2020). International Journal of Business and Management Invention (IJBMI), 20-27. |

[14]

. The study argues that the success of several women-owned micro-enterprise projects has a high association with reliable access to credit services. However, according to the authors, due to the prevalence of numerous socio-cultural practices, several of these projects fail to secure the required credit financing and consequently fail to meet their full potential. It is on this basis that the authors seek to establish the influence of socio-cultural practices on the credit uptake behavior of women-owned micro-enterprise projects. The sample taken is 504 women micro-entrepreneurs, 8 credit managers, 7 credit officers, and 2 county social development officials. The study reveals that a unit increase in the prevalence of socio-cultural practices reduces credit uptake among women enterprises by 32.7%.

Aura, A. J., in their study focus on subprime lending which the author described as the process of lending loans to borrowers at an above-prime rate

| [2] | Aura, A. J. (2020). THE EFFECTS OF SUBPRIME LENDING ON THE FINANCIAL PERFORMANCE OF SMALL BUSINESSES IN KENYA. A CASE STUDY OF KILIFI COUNTY. KILIFI. |

[2]

. The author noted that there has been a low volume of loan lending to small businesses despite a high number of subprime loan institutions. The study also argues that the low loan volume was because of the inherently risky nature of small business loans. The study thus seeks to investigate the effect subprime lending has on the financial performance of small businesses in Kilifi County.

Musebe uses multiple linear regression to assess the factors that influence demand for agricultural credit

| [24] | Musebe, N. V. (2020). ANALYSIS OF FACTORS INFLUENCING DEMAND FOR AGRICULTURAL CREDIT AMONG FARMERS IN KAPENGURIA, WEST POKOT COUNTY, KENYA. Eldoret: Moi University. |

[24]

. Based on the findings, the study recommends that financial services should be expanded through increasing agency banking, intensification of farmers' advisory services, developing initiatives to promote agricultural borrowing, coming up with loan products tailored to suit the small-scale farmers, and establishing special programs that will ensure credits for the purchase of product inputs are availed.

Another study investigates the relationship between the interest rate cap and access to credit by micro, small, and medium enterprises in Kisumu County, as it tries to answer the question of the effectiveness of interest rates in controlling the supply of money to MSMEs

| [30] | Osir Rosalyne Adhiambo, D. C. (2021). Relationship between Interest Rate Cap and Access to Credit by Micro, Small and Medium Enterprises in Kisumu County, Kenya. World Journal of Innovative Research (WJIR), 45-56. |

[30]

.

Based on the above studies and many others not listed here, it was evident that even though many studies have been conducted around loan services, there is a need to consider how the “non-loan” factors such as the Monthly expenditure per adult, Deposits, ESI and Diverse Economic Opportunities influence loan taking. This study therefore seeks to study key factors influencing the loan-taking habits among borrowers in Kenya.

3. Methodology

In this section, the authors describe the mathematical and statistical techniques and procedures used to identify and analyze information regarding the determinants of loan consumption in Kenya to achieve the objectives using the selected research instruments. The section outlines all the important aspects of research, including research design, data collection methods, data analysis methods, data interpretation and the overall contextual framework within which the research is conducted

. A comprehensive and structured methodology is necessary to provide a detailed and reliable analysis of the determinants of loan uptake in Kenya, contributing valuable insights for financial institutions, policymakers, and other stakeholders.

Study Design

Quantitative analysis is adopted to statistically analyze the relationship between various determinants and loan uptake using descriptive and inferential research methods. Descriptive research tries to describe a population attribute or phenomenon by summarizing the demographic and socio-economic characteristics of the target population

. The authors adopt this approach since they intend to come up with symmetric descriptions and analysis of the variables under investigation using frequency tables, graphs, trends, and other statistical tools such as measures of dispersion and central tendency and categories. The inferential method on the other hand allows the authors to use the sample data at hand to draw inferences about the population from which the dataset obtains

. It uses regression analysis to identify the determinants of loan consumption. A multiple linear regression analysis is adopted to determine the impact of various predictor variables (e.g., monthly expenditure per adult, deposits, economic strength index, and diverse economic opportunities) on the response variable (loan uptake).

Target Population

Identifying the appropriate target population is crucial for accurately studying the determinants of loan consumption in Kenya. The target population encompasses a diverse range of individuals and entities that reflect the broader Kenyan context. A target population is the whole population in which a researcher intends to carry out research and analysis

| [17] | Lavrakas, P. (2008). Encyclopedia of Survey Research Methods. Sage. Retrieved from djsresearch. |

[17]

. This is the population from which a sampling frame is drawn. A population in research methodology is an inclusive group of people, entities, objects, services, events, etc. that exhibit common characteristics that the research is being carried on

. In this study, the target population is the entire population of Kenya across all

counties. Kenya has a population of

million, distributed across

million households

| [6] | Central Bank of Kenya. (2019). Bank Supervision Annual Report 2019. |

[6]

. The target population for studying the determinants of loan consumption in Kenya is diverse, encompassing various demographic, socio-economic, and institutional segments. By carefully selecting a representative sample from these groups, the study can provide comprehensive insights into the variables influencing loan uptake, addressing the needs and challenges of different population segments

| [34] | Rehan Azam, M. D. (2012). The significance of socioeconomic factors on personal loan decision. Munich: Munich Personal RePEc Archive. |

[34]

.

Data Source

The study uses secondary data from the Kenya National Bureau of Statistics census. The data are aggregated at the county level, implying that the attributes that we are assessing are not for one individual respondent but the overall county parameters. To obtain the data, the authors compile Volume IV Kenya Population and Housing Census- Report, KIHBS--Basic Report on Well-Being in Kenya, and Kenya National Housing Survey Report . This is because different attributes could be found in different reports.

Data Cleaning and Processing

A data cleaning process is run after attainment of the data, to ensure that any error that may have an impact on the analysis is captured and corrected. The authors also ensure that the data is made in a format that is ready for analysis by coding any of the attributes that require coding to make sure that the data passing to the analysis stage is clean and ready to give the desired outcome.

Data Analysis

After compiling and cleaning the data, the authors use R, SPSS, and Excel to analyze the quantitative data. The authors adopt a descriptive analysis to help in describing several parameters of the variables under investigation using graphs, pie charts, and frequency tables.

In particular, the authors adopt an inferential analysis using multiple linear regression and stochastic linear regression to investigate the relationship between the response variable, Loan consumption, and the predictor variables; Monthly expenditure per adult, Deposits, ESI, and Diverse Economic Opportunities and assess the extent of which they influence the loan consumption.

The study is conducted at a significant level and the p-values of the test statistics for the respective predictor variables are compared against the significant level.

The decision criterion is to reject the null hypothesis if the is less than the significant level.

Multiple Linear regression model is a deterministic inferential technique that uses more than one explanatory variables in predicting the outcome of a response variable. Based on the authors specific objectives, four predictor variables are used to predict the outcome of loan consumption, making the multiple regression model the best fit for the prediction. The proposed multiple linear regression model is:

where;

Loan consumption (measured loan taken in the county)

Monthly expenditure per adult

Deposits made

Counties’ economic strength index

Counties’ diverse economic opportunities

error term

Therefore the regression estimate function is:

Table 1. Multiple linear regression assumptions.

Assumption | Explanation | Test |

Linear relationship | Dependent variable and independent variables exhibit a linear relationship | Scatter plot |

Independence | No correlation between the residuals | Residual plot |

Homoscedasticity | Constant variance | A scatterplot of residuals versus predicted values |

Normality of the residuals | The error between predicted values and observed values should be normally distributed | Shapiro-Wilk’s test |

No multi-collinearity | No high correlation between independent variables | Variance Inflation Factor |

Stochastic regression works like deterministic regression with the difference being that in stochastic regression, the explanatory variables are stochastic in nature, i.e., the explanatory variables allow for random variation in observations. To come up with a stochastic model, we run a Monte Carlo simulation and then regress the outcome data to obtain a stochastic regression model and establish how the deterministic prediction from the multiple linear regression model compares with the stochastic regression model that considers the error term.

4. Data Analysis and Interpretation

Descriptive analysis

Descriptive analysis provides a summary of the characteristics of the data collected, helping to identify patterns and trends within the target population. Descriptive analysis provides a comprehensive overview of the data collected, offering insights into the characteristics and behaviors of the target population concerning loan consumption. This analysis forms the foundation for more advanced statistical analyses and helps in understanding the broader context of loan uptake determinants in Kenya. The tables below give a summary description of the data under various variables in the study.

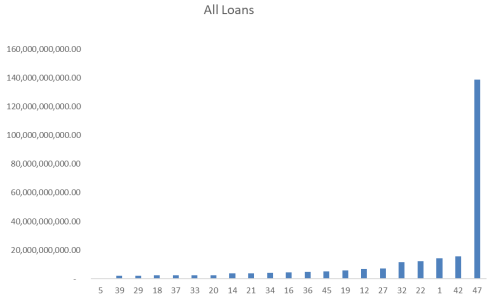

1. All Loans

Figure 1. Bar graph showing the distribution of loans across different counties.

Table 2. Descriptive table for all loans.

Mean | 5,932,695,287.64 |

Median | 1,923,111,624.00 |

Standard Deviation | 20,123,537,174.84 |

Range | 138,601,454,421.00 |

Minimum | 46,900,000.00 |

Maximum | 138,648,354,421.00 |

From the table, on overage, the loan obtained per county = 5,932,695,287.64, with a standard deviation of 20,123,537,174.84 the range between counties with the highest loan uptake and least loan uptake = 138,601,454,421.00.

The graph shows how the loan consumption is distributed across different counties. The county with the highest loan uptake is Nairobi County (County code 047). The majority of counties have their total loan consumption below Ksh. 20,000,000,000 with only three counties; Mombasa, Kisumu, and Nairobi having their cumulative loans above Ksh. 20,000,000,000.

2. Deposits

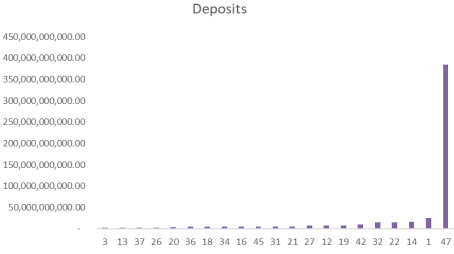

Figure 2. Bar graph showing the distribution of deposits across different counties.

Table 3. Descriptive table for deposits.

Mean | 11,849,429,639.87 |

Median | 1,641,000,000.00 |

Standard Deviation | 55,757,312,444.91 |

Range | 384,379,866,604.00 |

Minimum | 73,000,000.00 |

Maximum | 384,452,866,604.00 |

On overage, the money deposited per county = 11,849,429,639.87 Kenya shillings with a standard deviation of 55,757,312,444.91 the range between counties with highest deposits and least cash deposits = 384,379,866,604.00.

The graph shows how the cash deposits are distributed across different counties. The county with the highest deposit is Nairobi County (County code 047). The majority of counties have their total deposits below Ksh. 50,000,000,000 with only Nairobi County having cumulative deposits above Ksh. 50,000,000,000.

3. Monthly expenditure per adult

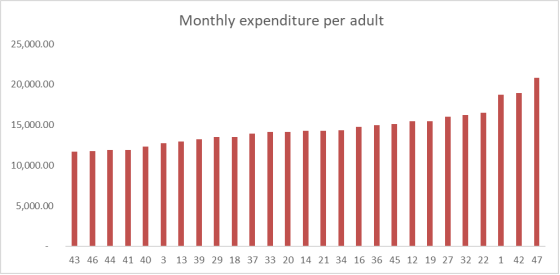

Table 4. Descriptive table for Monthly Expenditure per Adult.

Mean | 12,059.06 |

Median | 11,904.00 |

Standard Deviation | 3,752.24 |

Range | 16,107.25 |

Minimum | 4,690.00 |

Maximum | 20,797.25 |

Counties record an average monthly expenditure of 12,059.06 Kenya shillings with a standard deviation of 3,752.24. The monthly expenditure among the 47 counties is distributed over a range of 16,107.25 Kenya shillings. The minimum expenditure across all 47 counties is 4690 while the county with the highest adult monthly expenditure recorded 20,797.

Figure 3. Bar graph showing distribution Monthly Expenditure per Adult across different counties.

From the graph above, the majority of counties have a monthly adult expenditure lying between 10,000 and 20, 000 Kenyan shillings per month. Only Mombasa, Kisumu, and Nairobi have an average monthly adult expenditure above 20,000 Kenyan shillings.

4. Diverse Economic Opportunities

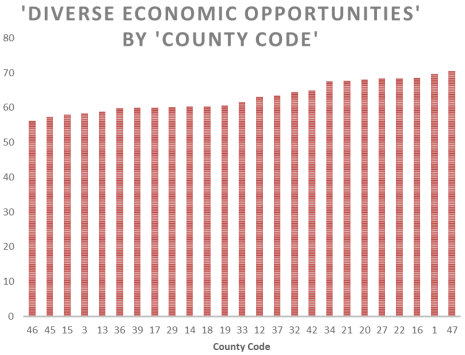

A Diverse economic opportunity is an index used to measure the economic diversity of a location. The authors describe economic diversity as how the economic status of a region varies. In other words, economic diversity can be described in terms of the range of economic activities available in a region. Diverse economic opportunities try to compare how economic activities vary in a given region. This is summarized in the table below:

Figure 4. Bar graph showing the distribution of Diverse Economic Opportunities across different counties.

Table 5. Descriptive table for Diverse Economic Opportunities.

Diverse Economic Opportunities |

Mean | 55.29 |

Median | 57.35 |

Mode | 60.06 |

Standard Deviation | 11.18 |

Range | 46.28 |

Minimum | 24.31 |

Maximum | 70.59 |

The mean diverse economic opportunity in Kenya is 55.29 with a standard deviation of 11.18. The most recorded diverse economic opportunity value is 60.06. The county with the lowest diverse economic opportunity score is 24.31 while the highest score is 70.59. The diverse economic score is spread across a range of 46.28.

The graph gives a visual presentation of the Diverse economic opportunity score distribution across different counties. The majority of the counties have an economic diversity score of between 50 and 70.

5. Economic Strength Index

The Economic Strength Index is an index used to measure the economic power of an area. This is measured based on how busy the economy of a place is and it is important in determining how an economy of a place is doing. The greater the ESI score the better the economy.

Below is the table showing a summary of the country’s ESI by county:

Table 6. Descriptive table for Economic Strength Index.

ESI |

Mean | 39.01 |

Median | 28.14 |

Standard Deviation | 26.03 |

Range | 85.70 |

Minimum | 10.48 |

Maximum | 96.18 |

From the table, the mean Economic strength index for the country is 39.01 with a standard deviation of 26.03. The scores are distributed across the range of 85.7 with the lowest recorded score being 10.48 and the highest being 96.18.

Comparing the mean and the median, it can be argued that the data is more skewed to the left, judging from the fact that there is a mean that is greater than the median.

Figure 5. Bar graph showing the distribution of the Economic Strength Index across different counties.

The bar graph above gives a vivid distribution of the Economic strength index across different counties. The graph omits the small values for clear visualization. It is noted that the majority of variables lie between 20 and 96, with Nairobi, Kiambu, Mombasa, Nakuru, and Machakos recording the highest ESI.

Multiple Linear Regression model

The authors apply a multiple linear regression model to analyze the relationship between the response and explanatory variables. In order to perform the analysis, they first explore the data to make sure that all the conditions for conducting the multiple linear regression are met.

Based on the descriptive analysis, it is vividly clear that our response variable show a skewed distribution. With some values such as the Nairobi County entries being very high, there might be a risk of outliers in our data. It is important to check for the outliers before running a multiple linear regression because even though the technique is usually robust and allows for disregard of assumptions to a certain level, it is usually sensitive to outliers. This implies that the presence of outliers pose the risk of obtaining wrong inferences that may mislead the study.

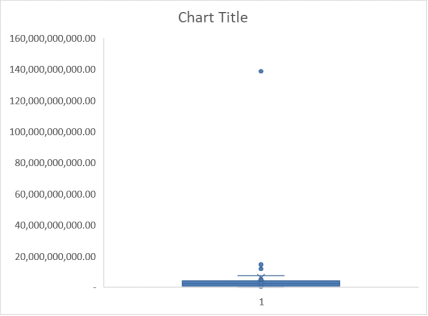

To confirm this, we first ran a boxplot of the response variable; loans, before proceeding to conduct the regression analysis.

Boxplot to check for outliers

Figure 6. Box plot for the whole dataset.

The box plot indicates the presence of outliers in the data, which are represented by the data points outside the box plot.

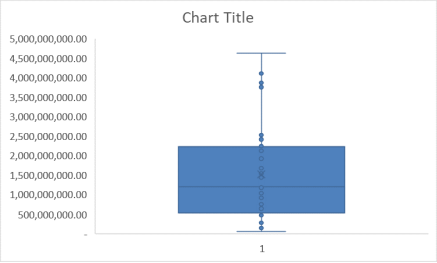

The skewness in the data is largely as a result of existing outliers. In order to continue with the regression analysis, the authors remove cases with outlier entries to remain with the section of the data without outliers as a way of treating outliers. The box plot below gives the distribution after the outliers are removed.

Figure 7. Box plot after removing outliers.

After removing the outliers, the data is still skewed to the right. However, the study can now continue with the tests for the assumptions of the multiple linear regression tests using the data without outliers.

Meanwhile, a test for the assumptions of a multiple linear regression model is employed.

1. Shapiro- Wilk’s test for Normality of the residuals

Below is the R output for Shapiro-Wilk's test for the normality of residuals

Shapiro-Wilk normality test

data: res1

W = 0.97059, p-value = 0.4247

To test for the normality of residual we formulate the hypothesis as follows:

H0: the residuals are normally distributed

H1: the residuals are not normally distributed

From the Shapiro-Wilk’s output, the Wald statistic and the . Since the -value is greater than our level of significant, we do not reject the null hypothesis, we therefore conclude that the data meets the assumption of normality of the residuals.

2. Linear relationship between the response variables and explanatory variables assumption

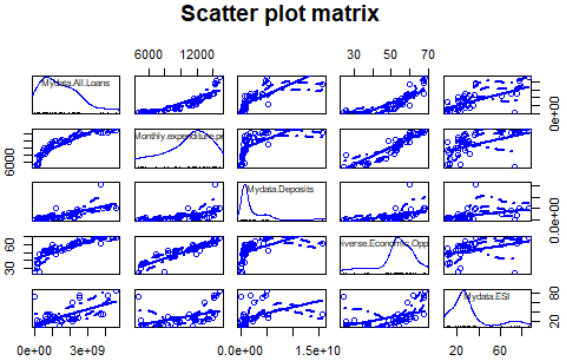

To test for this linear relationship, we plot the scatter plot for the response versus explanatory variables as given below:

Figure 8. Scatter matrix for test for linearity.

The relationship between Loans and the independent variables; Monthly expenditure, Deposits, Diverse economic opportunities, and ESI is investigated.

This relationship can be shown by the first column of our scatter plot. From the second row of the first column, there exists a linear relationship between Loans and Monthly expenditures. There is also a linear relationship between deposits and loans based on the third row of the first column of our scatter matrix. Finally, the fourth and fifth rows show that there exists a linear relationship between loans and diverse economic opportunities and loan and ESI, respectively.

Based on our assessment of the scatter matrix, we can therefore say that the linear relationship assumption is met.

3. The Independence assumption

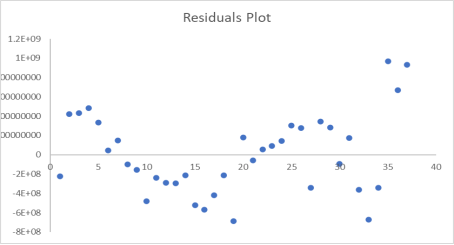

Another assumption of the multiple linear regression model is that the observations in the data are selected independently of each other.

In order to test for the assumption that observations are independent of each other, the authors plot the residual plot. From the scatter plot above, there is no clear pattern exhibited by the residuals. This implies that there is no association between one residual and another. This therefore means that there is no dependence between the observations. In conclusion, the authors assert that the data meets the assumption of independence.

Figure 9. Scatter plot for test for independence.

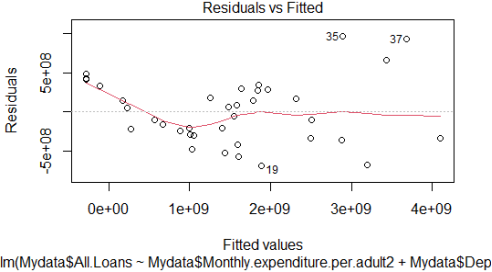

4. Homoscedasticity

The assumption constant variance is tested. This assumption describes the situation where the variance in the relationship between the response and the explanatory variables is the same. A scatter plot of the residuals versus fitted values is used for measurement.

The scatter plot below gives the output test output:

Figure 10. Residuals versus fitted values for testing for Homoscedasticity.

From the plot above, it is evident that there is no clear pattern formed by the residuals. This implies that the error term of the relationship between the response and the explanatory is approximately constant across all values of the independent variables.

In essence, the data meets the assumption of constant variance.

5. No multicollinearity assumption

Finally, the assumption of multicollinearity is tested. This assumption indicates that there should be no linear relationship between two independent variables. To perform this test, the authors use Pearson’s correlation matrix of the explanatory variables. The outputs are as shown in the table below:

Table 7. Correlation matrix table for testing for multi-collinearity.

| Deposits | Monthly expenditure per adult2 | ESI | Diverse Economic Opportunities |

Deposits | 1 | | | |

Monthly expenditure per adult2 | 0.358160621 | 1 | | |

ESI | 0.152847234 | 0.249778429 | 1 | |

Diverse Economic Opportunities | 0.267572029 | 0.305360956 | 0.387969144 | 1 |

From the correlation matrix table, the correlation between any pair of independent variables gives a weak correlation. Since all the variables are giving weak correlation, we can say that despite the association, it is too weak to raise concern. Therefore, the data exhibits little linear association among the independent variables hence the authors conclude that the assumption of multicollinearity is met.

All the assumptions required in conducting a multiple linear regression analysis have been tested, and found the data meeting all the assumptions.

5. Results

Results for the multiple linear regression model analysis

Recall that the response variable is the total loans in a county and the predictor variables are Deposits, Monthly expenditure per adult, Economic Strength Index of the counties, and counties' Diverse Economic Opportunity scores.

We ran the linear regression model to assess the relationship between the response variable and our explanatory variables to answer research questions. The results are presented in the table below:

Table 8. Regression statistics table.

Regression Statistics |

Multiple R | 0.938262295 |

R Square | 0.880336135 |

Adjusted R Square | 0.865378152 |

Standard Error | 438911674.6 |

Observations | 37 |

Table 9. ANOVA table for fitness of the model.

ANOVA | df | SS | MS | F | p-value |

Regression | 4 | 4.53513E+19 | 1.13E+19 | 58.85393287 | 2.67E-14 |

Residual | 32 | 6.16459E+18 | 1.93E+17 | | |

Total | 36 | 5.15159E+19 | | | |

Call:

Lm (formula = All Loans ~ Monthly expenditure per adult2 +Deposits + Diverse Economic Opportunities +ESI)

Residuals:

Table 10.

Summary descriptive table of the residuals. Summary descriptive table of the residuals. Summary descriptive table of the residuals. Min | First Quartile | Median | Third quartile | Max |

-687553837 | -296325379 | -60430568 | 2.8E+08 | 9.7E+08 |

Table 11. Summary table of coefficients.

| Coefficients: | Estimate Std. Error | t value | Pr (>|t|) |

(Intercept) | -2055000000.00 | 387000000.00 | -5.31 | 8.07e-06 *** |

Monthly expenditure per adult | 182000.00 | 61450.00 | 2.96 | 0.005733 ** |

Deposits | 0.13 | 0.03 | 4.05 | 0.000303 *** |

Diverse Economic Opportunities | 17130000.00 | 15560000.00 | 1.10 | 0.27895 |

ESI | 14230000.00 | 4085000.00 | 3.48 | 0.001455 ** |

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

From the output above, the following interpretations are made:

There is a strong association between the explanatory variables and the response variable as shown by the . implies that of the variations in loan consumption are explained in the model.

The ANOVA table gives the overall suitability of the model. From the ANOVA table with a . Since the is less than , we conclude that the model is suitable enough to predict the loan consumption.

The error terms associated with the model are distributed with a minimum of and a maximum of .

Recall the hypotheses:

: Monthly expenditure per adult has no significant effect on loan consumption in Kenya.

: Deposit has no significant effect on loan consumption in Kenya.

: The Economic Strength Index (ESI) has no significant effect on loan consumption in Kenya.

: Diverse Economic Opportunities (DEO) have no significant effect on loan consumption in Kenya.

For Monthly expenditure per adult, with . Since the is less than the significant level of , the null hypothesis is rejected and the authors conclude that Monthly expenditure per adult has a significant effect on loan consumption in Kenya.

For deposits, with . Since the is less than the significant level of , the null hypothesis is rejected and the authors conclude that deposits have a significant effect on loan consumption in Kenya.

For ESI, with . Since the is less than the significant level of , the null hypothesis is rejected and the authors conclude that ESI has a significant effect on loan consumption in Kenya.

Diverse Economic Opportunities, with . Since the is greater than the significant level of , the null hypothesis is not rejected and the authors conclude that Diverse Economic Opportunities have no significant effect on loan consumption in Kenya.

Results for the stochastic regression model analysis

A stochastic regression model analysis is carried out to assess how the stochastic modeling compares to the deterministic modeling. It is recalled that as opposed to the linear regression model which is deterministic, the stochastic model allows for random variation in the variables input in the model.

To induce the random variation aspect, the authors conduct a Monte Carlo simulation. The output below is the linear regression output after running the Monte Carlo simulation:

Table 12. Linear regression output table.

Number of obs | 37 |

Replications | 100 |

Wald chi2(4) | 175.56 |

Prob > chi2 | 0.0000 |

R-squared | 0.8807 |

Adj R-squared | 0.8658 |

Root MSE | 4.38e+08 |

Table 13. Stochastic regression summary table.

All loans | Observed Coef. | Bootstrap Std. Err. | z | P>|z| | Normal [95% Conf. Interval] |

Deposits | 0.13 | 0.084724 | 1.5 | 0.135 | -0.0392841 | 0.292826 |

Monthly expe | 181411.50 | 47718.26 | 3.8 | 0 | 87885.46 | 274937.6 |

| 14200000.00 | 5920214 | 2.4 | 0.016 | 2627466 | 2.58E+07 |

Diverse Econ | 17200000.00 | 1.61E+07 | 1.07 | 0.286 | -1.44E+07 | 4.87E+07 |

_cons | -2050000000.00 | 5.39E+08 | -3.81 | 0 | -3.11E+09 | -9.95E+08 |

From the outputs, The Wald chi-squared, with . This implies that the model is good enough to be used in predicting the response variable.

The Adjusted while the adjusted for the previous multiple regression model is . The difference in is very small implying that the extra variation in the stochastic model not explained in the previous model is very minimal.

Due to the consideration of the error term in the stochastic model, the coefficients of independent variables are slightly higher in the stochastic model compared to the deterministic model.

Deposits and Diverse Economic Opportunities are both not statistically significant in the stochastic model while only Diverse Economic Opportunities is not statistically significant in the deterministic model.

6. Discussions

The study investigates if:

a). Monthly expenditure per adult is significant in determining the loan consumption in Kenya

b). Deposit is significant in determining the loan consumption in Kenya,

c). Economic Strength Index (ESI) is significant in determining the loan consumption in Kenya and

d). Diverse Economic Opportunities (DEO) are significant in determining the loan consumption in Kenya.

These objectives were fulfilled by the multiple linear regression model analysis shown earlier.

From the linear output, factors with significant effect in predicting loan consumption which are monthly expenditure per adult, ESI, and deposits are obtained. From the output, the model is presented as follows:

It is noted that MEpA is the monthly expenditure per adult and ESI is the economic strength index. Diverse economic opportunity is not statistically significant and thus not included in our final model.

Model Explanation

When all the independent variables are at zero, the total loan consumption will be -2055000000. An increase in monthly expenditure per adult by one shilling given other factors are held constant, is likely to increase the total loan uptake amount by 182,000 shillings. An increase in deposit amount by one shilling given other factors being held constant increases the loan consumption by 0.13 shillings. Finally, the county with a one-unit higher ESI is likely to have 14230000 shillings higher loan consumption compared to the county with lower ESI.

From the comparison of the two tables, it is observed that the adjusted of multiple linear regression is 0.8653 which is approximately equal to the adjusted R-squared for the stochastic regression model which is 0.8658. This implies that there are no significant variations explained by the stochastic model that are not explained by the linear regression model.

Comparing the study findings and some of the empirical studies discussed in the literature review, it is evident that the results align with the majority of the studies. Based on the study results, monthly expenditure per adult, deposits, and economic strength index are found to significantly impact the loan consumption amount. The findings provide further assurance of the importance of these factors in understanding loan consumption characteristics. These findings and the study’s contribution to the understanding of loan consumption characteristics in Kenya are consistent with the broader literature, revealing relevant insights about key stakeholders involved in lending and borrowing processes.

For instance, the study obtains a significant impact of monthly expenditure per adult in determining loan consumption, which is consistent with the previous literature review studies that obtain a correlation between economic status and loan demand. The use of quantitative analysis, such as the deterministic multiple linear regression and stochastic analysis through Monte Carlo simulation offer a rigorous methodological approach that enriches and broadens the existing research methodologies employed in similar studies.

The study also reveals a consistent pattern with other studies discussed in the literature review in supporting the impact the economic factors have on loan consumption. The emphasis that the study puts on the economic strength index also aligns with the previous research works that highlight the role of economic conditions in shaping borrowing characteristics. Also, the study's examination of the impact of diverse economic opportunities on loan consumption aligns with literature emphasizing the relationship between entrepreneurial activities and access to credit.

Based on this analysis between the study findings and empirical studies discussed in the literature review, it is evident that this study adds depth to the existing body of knowledge on the determinants of loan consumption in Kenya. This study therefore enriches our understanding of the complex relationship between economic variables and loan consumption behaviors.

Model Limitation

From the model analysis, the authors observe that there is a possibility of obtaining negative loan consumption. However, in real life situations, Loan consumption is a non-negative continuous random variable. This negativity is brought about by the fact that this study is working with aggregated data and not individual borrowers. That is, instead of using the records of borrowers at the individual level, the authors use the data as aggregated at the county level, which might not be wholly representative of the true situation.

The data might also be the reason why very huge coefficients of the predictor variables are obtained.

7. Conclusions and Recommendations

The objective of this study is to examine the determinants of loan consumption in Kenya, giving more attention to four variables which are monthly expenditure per adult, deposits, economic strength index, and the diverse economic opportunity.

To assess the relationship between the variables and loan consumption, the authors run a multiple linear regression model analysis with loan consumption as the response variable and monthly expenditure per adult, deposits, ESI, and diverse economic opportunity as the predictor variables. From the model analysis, the authors establish that monthly expenditure per adult, economic strength index, and deposits significantly influence the loan uptake. Further, the model results indicate that 88% of the variations in loan uptake are explained by the predictor variables, implying that about 12% of the variation in loan uptake is explained by other variables not discussed in the study.

This study recommends the following:

1. More emphasis to be made on the deposits, monthly expenditure per adult, and economic strength index when considering new markets for financial lending institutions.

2. Further study to be conducted on how lending can improve the economic status of the borrowers. This is because with the rise in economic status, comes a rise in economic activities individuals are involved in thus likelihood of higher borrowing and repayment rates.

3. Further study can also be conducted on other potential variables associated with loan consumption, as this study does not explain all the variables that are related to loan consumption.

4. The authors also recommend that a further study be carried out on a similar topic area but using individual borrower records and not aggregated data as in the case of this survey.

Abbreviations

MSME | Micro, Small and Medium Enterprises |

ANOVA | Analysis of Variance |

ESI | Economic Strength Index |

GOK | Government of Kenya |

MEpA | Monthly Expenditure Per Adult |

Acknowledgments

The authors would like to thank the contributions of the assigned Science Publishing Group (AJTAS) editors Daniel Williams, Judy Garland, Oliver Phillips and the two anonymous reviewers whose comments helped to improve the manuscript greatly.

Author Contributions

Conlet Biketi Kikechi: Conceptualization, Methodology, Data curation, Formal analysis, Resources, Software, Supervision, Validation and writing the original draft

Dau Malek Dau: Conceptualization, Methodology, Investigation, Data curation, Formal analysis, Resources, Software, Supervision, Validation and writing the review and editing

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] |

Agarwal, P. (2018, February 14). Liquidity Preference Theory. Retrieved from Inteligent Economist:

https://www.intelligenteconomist.com/liquidity-preference-theory/

|

| [2] |

Aura, A. J. (2020). THE EFFECTS OF SUBPRIME LENDING ON THE FINANCIAL PERFORMANCE OF SMALL BUSINESSES IN KENYA. A CASE STUDY OF KILIFI COUNTY. KILIFI.

|

| [3] |

Beck, T., Demirguc-Kunt, A., & Martinez Peria, M. S. (2008). Banking Services for Everyone? Barriers to Bank Access and Use around the World. World Bank Economic Review, 22(3), 397-430.

|

| [4] |

Bryce. (2003). Descriptive & Inferential Statistics: Definition, Differences & Examples. Retrieved from Study. com:

https://study.com/academy/lesson/descriptive-and-inferential-statistics.html

|

| [5] |

Central Bank of Kenya. (2017). THE BANKING (PENALTIES) REGULATIONS, 2017. Nairobi: Central bank of Kenya.

|

| [6] |

Central Bank of Kenya. (2019). Bank Supervision Annual Report 2019.

|

| [7] |

Finaccess. (2015, September). FinAccess Business – Supply Bank Financing of SMEs in Kenya. Retrieved from Central Bank of Kenya:

https://www.centralbank.go.ke/images/docs/Bank%20Supervision%20Reports/BankFinancingSMEsKenya.pdf

|

| [8] |

Financial Sector Deepening (FSD) Kenya. (2014). The Growth of M-Shwari in Kenya – A Market Development Story.

|

| [9] |

Financial Stability Review. (2009, June). Determinants of Bank lending standards and the impact of the financial turmoil. Retrieved from

https://www.ecb.europa.eu/pub/pdf/fsr/art/ecb.fsrart200906_01.en.pdf

|

| [10] |

Guided Choice. (2021). Harry Markowitz’s Modern Portfolio Theory: The Efficient Frontier. Retrieved from Guided Choice:

https://www.guidedchoice.com/video/dr-harry-markowitz-father-of-modern-portfolio-theory/

|

| [11] |

Government of Kenya (GOK). (2018). Economic Survey 2018.

|

| [12] |

Hivos People Unlimited. (2016, June). Kenya’s Efforts to Empower Women, Youth, and Persons with. Retrieved from Hivos People Unlimited:

https://www.openupcontracting.org/assets/2018/04/Agpo-Report-Web-version-Full-Report.pdf

|

| [13] |

Isoraite, M. (2008). THE BALANCED SCORECARD METHOD: FROM THEORY TO PRACTICE. INTELLECTUAL ECONOMICS, 18-28.

|

| [14] |

James MutukuNzeki, D. G. (2020). International Journal of Business and Management Invention (IJBMI), 20-27.

|

| [15] |

Johnson, S., & Arnold, S. (2012). Inclusive Financial Markets: Is Transformation Underway in Kenya? Development Policy Review, 30(6), 719-748.

|

| [16] |

Kumar, M. (2018). Loanable Funds Theory (With Diagram). Washington DC: Economics discussion.

|

| [17] |

Lavrakas, P. (2008). Encyclopedia of Survey Research Methods. Sage. Retrieved from djsresearch.

|

| [18] |

Linda Ghent, A. G. (2010). Concept: imperfect information. Retrieved from The Economics of Seinfeld:

https://www.yadayadayadaecon.com/concept/imperfect-information/#:~:text=Imperfect%20information%20is%20a%20situation,are%20more%20familiar%20with%20it

|

| [19] |

Maina, K. (2014). Assessing Institutional Factors contributing to loan defaulting in MFIs in Kenya. Nairobi.

|

| [20] |

Makorere. (2014). Factors Affecting loan default in Tanzania. Daresalam.

|

| [21] |

Mbiti, I., & Weil, D. N. (2011). Mobile Banking: The Impact of M-Pesa in Kenya. NBER Working Paper No. 17129.

|

| [22] |

McCombes, S. (2019, May 15). Descriptive research. Retrieved from Scribbr:

https://www.scribbr.com/methodology/descriptive-research/#:~:text=Descriptive%20research%20aims%20to%20accurately,investigate%20one%20or%20more%20variables

|

| [23] |

McCombes, S. (2019, February 25). How to write a methodology. Retrieved from Scribbr:

https://www.scribbr.co.uk/thesis-dissertation/methodology/

|

| [24] |

Musebe, N. V. (2020). ANALYSIS OF FACTORS INFLUENCING DEMAND FOR AGRICULTURAL CREDIT AMONG FARMERS IN KAPENGURIA, WEST POKOT COUNTY, KENYA. Eldoret: Moi University.

|

| [25] |

Mutezo. (2005). Obstacles in the access to SMME finance. Pretoria: University of South Africa.

|

| [26] |

Neziroglu, F. (2012, January 25). Hoarding: The Basics. Retrieved from ADAA:

https://adaa.org/understanding-anxiety/obsessive-compulsive-disorder-ocd/hoarding-basics#:~:text=Hoarding%20is%20the%20persistent%20difficulty,a%20hoarder%20and%20family%20members

|

| [27] |

Obiero, S. O. (2020). Influence of Women Enterprise Fund on Socio-Economic Development; A case study of Lurambi Constituency. Nairobi: University of Nairobi.

|

| [28] |

Ochung. (2013). Factors affecting loan repayment among customers of Commercial banks in Kenya. Retrieved from erepository:

http://erepository.uonbi.ac.ke/bitstream/handle/11295/56493/Factors%20Affecting%20Loan%20Repayment%20Among%20Customers%20Of%20Commercial%20Banks%20In%20Kenya%20A%20Case%20Of%20Barclays%20Bank%20Of%20Kenya%20Nairobi%20County.pdf?sequence=3

|

| [29] |

Olweny, E. K. (2015, June 4). FACTORS INFLUENCING LOAN UPTAKE RATE FROM COMMERCIAL BANKS BY CIVIL SERVANTS IN KENYA: A CASE OF MINISTRY OF EDUCATION HEADQUATERS. Retrieved from SEAHI:

https://seahipaj.org/journals-ci/june-2015/IJISSHR/full/IJISSHR-J-6-2015.pdf

|

| [30] |

Osir Rosalyne Adhiambo, D. C. (2021). Relationship between Interest Rate Cap and Access to Credit by Micro, Small and Medium Enterprises in Kisumu County, Kenya. World Journal of Innovative Research (WJIR), 45-56.

|

| [31] |

Pettinger, T. (2005, May). Asymmetric information problem. Retrieved from Economics Help:

https://www.economicshelp.org/blog/glossary/asymmetric-information/#:~:text=Asymmetric%20information%20can%20lead%20to,how%20reliable%20the%20engine%20is

|

| [32] |

Priscilla N. Wangai, B. M. (2011). Factors that Influence the Demand for Credit for Credit Among SmallScale Investors: a case study of Meru Central District, Kenya. Retrieved from

https://core.ac.uk/download/pdf/234629179.pdf

|

| [33] |

Rafeedalie, D. (2011, June 2). Research: Population and Sample. Retrieved from Top Hat:

https://tophat.com/marketplace/social-science/education/course-notes/oer-research-population-and-sample-dr-rafeedalie/1196/34349/

|

| [34] |

Rehan Azam, M. D. (2012). The significance of socioeconomic factors on personal loan decision. Munich: Munich Personal RePEc Archive.

|

| [35] |

Syomane, Felix S.; Dr. Michael, Wahome;. (2018). Financial Institutions Factors Influencing Loan Default by SMEs in Kitui County. Nairobi: INTERNATIONAL JOURNAL.

|

| [36] |

Tilly, G. (2006). Keyne's theory of liquidity preference and his debt management and monetary policies. Cambridge journal of Economics, 657-670.

|

| [37] |

Tram Nguyen, D. T. (2018, January 26). Operational Efficiency of Bank loans and Deposits; A case study of Vietnamese Banking system. Retrieved from ResearchGate:

https://www.researchgate.net/publication/284374676_Factors_Influencing_Loan_Repayment_in_Micro-Finance_Institutions_in_Kenya

|

| [38] |

Viffa Consult. (2019, November). KENYA SME PERFORMANCE INDEX 2019. Retrieved from

http://viffaconsult.co.ke/wp-content/uploads/2019/12/KENYA-SME-PERFORMANCE-INDEX-2019.pdf

|

| [39] |

Weiss. (2008). Credit Rationing in rural India. Journal of Economic Development, 23-45.

|

| [40] |

Weliver, D. (2021, March 19). How to Invest Money; the best way to make your money grow. Retrieved from Money Under 30:

https://www.moneyunder30.com/how-to-invest

|

Cite This Article

-

APA Style

Kikechi, C. B., Dau, D. M. (2024). Application of Deterministic Multiple Linear Regression and Stochastic Analysis Through Monte Carlo Simulation to Model Loan Consumption Assuming Kenyan Data. American Journal of Theoretical and Applied Statistics, 13(5), 138-156. https://doi.org/10.11648/j.ajtas.20241305.14

Copy

|

Copy

|

Download

Download

ACS Style

Kikechi, C. B.; Dau, D. M. Application of Deterministic Multiple Linear Regression and Stochastic Analysis Through Monte Carlo Simulation to Model Loan Consumption Assuming Kenyan Data. Am. J. Theor. Appl. Stat. 2024, 13(5), 138-156. doi: 10.11648/j.ajtas.20241305.14

Copy

|

Download

AMA Style

Kikechi CB, Dau DM. Application of Deterministic Multiple Linear Regression and Stochastic Analysis Through Monte Carlo Simulation to Model Loan Consumption Assuming Kenyan Data. Am J Theor Appl Stat. 2024;13(5):138-156. doi: 10.11648/j.ajtas.20241305.14

Copy

|

Download

-

@article{10.11648/j.ajtas.20241305.14,

author = {Conlet Biketi Kikechi and Dau Malek Dau},

title = {Application of Deterministic Multiple Linear Regression and Stochastic Analysis Through Monte Carlo Simulation to Model Loan Consumption Assuming Kenyan Data

},

journal = {American Journal of Theoretical and Applied Statistics},

volume = {13},

number = {5},

pages = {138-156},

doi = {10.11648/j.ajtas.20241305.14},

url = {https://doi.org/10.11648/j.ajtas.20241305.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ajtas.20241305.14},

abstract = {The main focus of this survey is to examine the key determinants of loan consumption in Kenya, with a keen focus on variables such as monthly expenditure per adult, deposits, economic strength index, and diverse economic opportunities. The study's target population is Kenyan citizens aged 18 years and above. The study obtains data from the Kenya national census, aggregated at the county level. The literature review section presents sufficient support for the study’s hypothesis. In particular, the authors highlight Kenya as a country with one of the highest loan consumption in Africa, which plays as a motivation for conducting this survey. The survey methodology involves the use of quantitative analysis using descriptive statistics like tables, graphs and charts, deterministic multiple linear regression, and stochastic analysis through Monte Carlo simulation. The results of the survey show that monthly expenditure per adult, deposits, and economic strength index have a significant impact on loan consumption amount; that is, R-squared is equal to 0.88. The implication of this survey is based on its contribution to the understanding of loan consumption behaviors in Kenya, presenting relevant insights for policymakers, financial institutions, and other stakeholders in the lending and borrowing processes. The outcome has the potential to inform loan structure policies to enhance the promotion of responsible and sustainable loan consumption.

},

year = {2024}

}

Copy

|

Download

-

TY - JOUR

T1 - Application of Deterministic Multiple Linear Regression and Stochastic Analysis Through Monte Carlo Simulation to Model Loan Consumption Assuming Kenyan Data

AU - Conlet Biketi Kikechi

AU - Dau Malek Dau

Y1 - 2024/10/18

PY - 2024

N1 - https://doi.org/10.11648/j.ajtas.20241305.14

DO - 10.11648/j.ajtas.20241305.14

T2 - American Journal of Theoretical and Applied Statistics

JF - American Journal of Theoretical and Applied Statistics

JO - American Journal of Theoretical and Applied Statistics

SP - 138

EP - 156

PB - Science Publishing Group

SN - 2326-9006

UR - https://doi.org/10.11648/j.ajtas.20241305.14

AB - The main focus of this survey is to examine the key determinants of loan consumption in Kenya, with a keen focus on variables such as monthly expenditure per adult, deposits, economic strength index, and diverse economic opportunities. The study's target population is Kenyan citizens aged 18 years and above. The study obtains data from the Kenya national census, aggregated at the county level. The literature review section presents sufficient support for the study’s hypothesis. In particular, the authors highlight Kenya as a country with one of the highest loan consumption in Africa, which plays as a motivation for conducting this survey. The survey methodology involves the use of quantitative analysis using descriptive statistics like tables, graphs and charts, deterministic multiple linear regression, and stochastic analysis through Monte Carlo simulation. The results of the survey show that monthly expenditure per adult, deposits, and economic strength index have a significant impact on loan consumption amount; that is, R-squared is equal to 0.88. The implication of this survey is based on its contribution to the understanding of loan consumption behaviors in Kenya, presenting relevant insights for policymakers, financial institutions, and other stakeholders in the lending and borrowing processes. The outcome has the potential to inform loan structure policies to enhance the promotion of responsible and sustainable loan consumption.

VL - 13

IS - 5

ER -

Copy

|

Download